One connected stack for

systematic investment workflows.

MethodTech connects risk modelling, alpha creation, portfolio construction, strategy testing, analytics, and wealth portfolio intelligence into one workflow for modern investment teams.

Scroll to explore

Risk Model

Understand Risk

Alpha Machine

Build Signals

Portfolio Construction

Optimise Portfolios

Strategy Builder

Test Strategies

Wealth Management

Serve Clients

Analytics

Explain Outcomes

Products

How MethodTech Fits Into the Investment Process

Risk Model

Alpha Machine

Portfolio Construction

Strategy Builder

Analytics

Wealth Management

Understand factor regimes. Diagnose every stock.

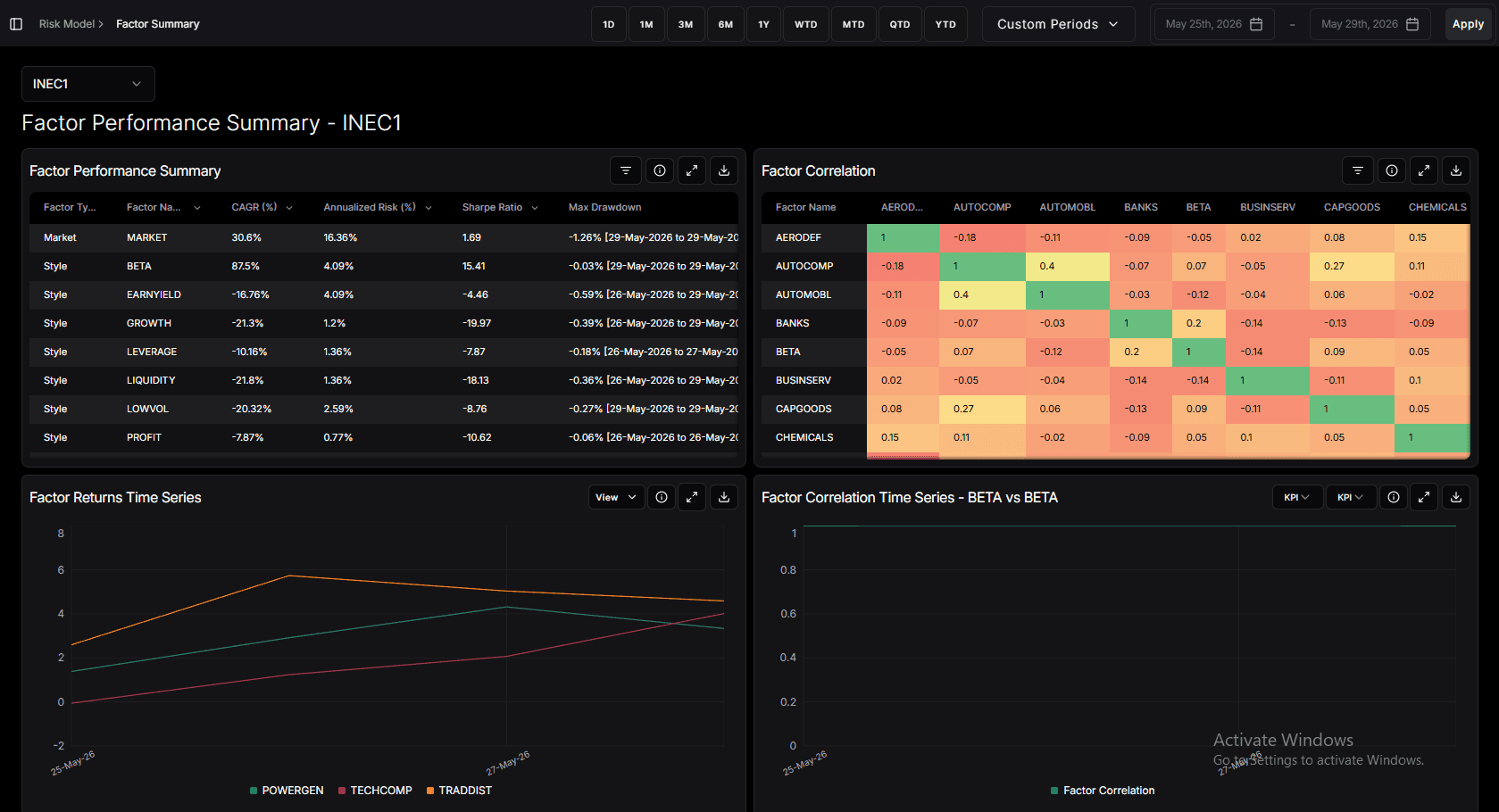

MethodTech’s Risk Model dashboard gives investment teams a deep view of how factors behave over time and how those factors explain stock-level returns and risks. Track long-term factor performance, volatility, drawdowns, and correlations, then drill down into every listed company to understand its factor exposures, idiosyncratic risk, predicted risk, and return decomposition.

Risk is not just a portfolio number. It starts with the behaviour of underlying factors and how each stock loads onto them.

MethodTech’s Risk Model dashboard helps teams study the market through a factor lens. Users can analyse long-term returns across style and industry factors, compare factor volatility, review maximum drawdowns, study factor correlations on any date, and track how those correlations evolve through time.

The same framework extends to the stock level. For every listed entity, MethodTech shows how much of the stock’s risk comes from systematic factor exposure versus idiosyncratic risk. It also decomposes historical stock returns into factor-driven and stock-specific components, helping teams understand whether performance came from beta, momentum, value, growth, industry exposure, or true stock-specific movement.

This turns the Risk Model into a practical research and diagnostics layer for PMs, analysts, quant teams, and risk teams. It helps them understand factor regimes, compare stocks through a common risk lens, and separate what the market rewarded from what the company itself delivered.

What It Helps You Do

Analyse long-term factor returns across market, style, and industry factors

Compare factor volatility, maximum drawdowns, and behaviour across regimes

Study factor correlation matrices on any selected date

Track time-series changes in factor correlations

View stock-level factor exposures for every listed company

Break each stock’s risk into factor risk and idiosyncratic risk

Decompose stock returns into factor-driven and stock-specific components

Track return decomposition over time across factors such as beta, value, growth, momentum, and industry exposures

Review factor loadings, predicted risk, and risk decomposition at the security level